Higher dividends - New group name - New Swatch responsible

Questo comunicato non è disponibile in italiano. Voglia consultare la versione inglese (qui di seguito) o la versione tedesca.

![]()

Biel / Bienne (Switzerland), 19 February 1998 - At yesterday`s meeting, the Board of Directors of the SWATCH GROUP Ltd, Biel (Switzerland) was duly notified of the provisional 1997 results for the SWATCH GROUP.

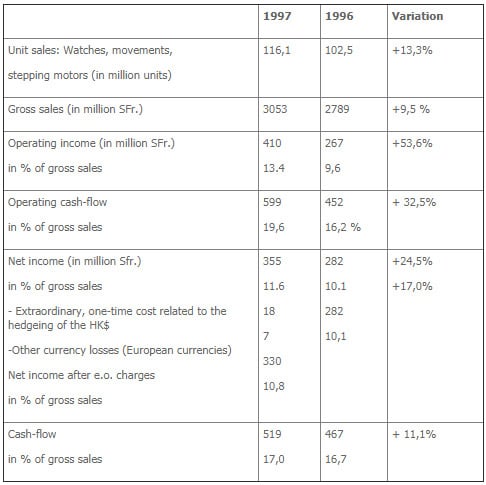

1. The group`s operations have developed as follows:

Net income (+ 17%) was unable to match the rise in operating profit (+53,6%) for the following reasons:

a) In order to hedge its position in Hong Kong and with particular regard to the possible repercussions of the colony’s return to Chinese rule in June/July 1997, which at that time were impossible to predict at the end of 1996, the SWATCH GROUP hedged its entire foreign currency position in Hong Kong dollars on the advice of its financial advisors. This generated hedgeing costs of around Sfr. 18 million.

b) The adverse currency movements reduced the financial income of the bond portfolio.

c) As expected, the tax rate has increased.

2. Higher dividend

In the light of the good performance in 1997 and the positive outlook for the current year, the Board of Directors has decided to propose to the General Meeting of Shareholders in June a dividend increase from last year’s figure of 18% to 20%.

3. 1998 Outlook

1997 was characterised by accelerated growth in the second half of the year and strong Christmas trading. All of the company`s brand-name products contributed to the increase in turnover whilst private label business - the manufacture of watches on behalf of third parties -showed a decrease. Marked progress was also made in certain areas of production and technology. This core business area - together with the microelectronics (EM-Marin) and battery (Renata) divisions - is to be expanded significantly through a targeted investment program. In today`s meeting, the Board of Directors has also approved the extensive expansion plans of these two fields of activities.

Despite the crisis in Asia, the Group continued its growth pattern in January and this upward trend is expected to continue in February.

4. New group name

At today`s meeting, the Board of Directors decided to propose to the General Meeting of Shareholders to change the name SMH in „The Swatch Group of Switzerland S.A." or into another name including the name „Swatch". The Group Management Board has been asked to submit proposals. The name SMH is very complicated and the abbreviation is difficult to understand in the various main languages. With the choice of „Swatch" added in the group`s name, the worldwide notoriety of the brand is taken into consideration.

5. New Swatch brand responsible

Moreover, the Board of Directors has appointed Mr. G.N. Hayek jun (up to now Vice-President Marketing of Swatch) General Manager and responsible of the watch brand Swatch Ltd. Mr. Hayek jun will maintain his functions with on the Group Management Board for Italy and Spain.

6. Share repurchase program / Reduction of equity

6.1 General

As mentioned earlier at various occasions, the Board of Directors has analysed the SWATCH GROUP`s substantial undisclosed reserves in the form of plant and machinery, real estate and premises, brand names and licences. With a view to implementing the firm commitment to continually and actively managing the group`s solid capital base, the Board of Directors has also resolved, in a first tranche, to repurchase its own shares up to a approximately 10% of its current market capitalisation. The proposed share repurchase program will include both registered shares with a nominal value of CHF 10 each and bearer shares with a nominal value of CHF 50 each in equal numbers and thus in proportion to their respective nominal values. The General Meeting of Shareholders of 24 June 1998 will be asked to approve a proposed capital reduction corresponding to the amount of the repurchase at that time.

The size of the first tranche was determined primarily by the amount of liquidity available after allowing for immediate operational requirements and provides adequate scope for organic growth and complementary acquisitions. The Board of Directors reserves the right to suspend or discontinue entirely the share repurchase programme in the event of a significant change in the operating environment. Provision has also been made for the possible extension of the program in the framework of an active balance sheet management strategy.

The share repurchase program will have a positive impact on both return on equity and earnings per share. The Board of Directors thus firmly believes that a share repurchase for the purpose of a capital reduction will be to the advantage of all shareholders. However, this does not constitute a general recommendation of participation in the programme on the part of The SWATCH GROUP Board. Shareholders are also advised to consider their individual tax implications.

The repurchase of SWATCH GROUP shares will be effected on the Swiss Stock Exchange by means of a second line of trading for bearer shares and another for registered shares, each established specifically for this purpose. The repurchase price in this additional second line of trading, in which The SWATCH GROUP alone may purchase shares, is likely to be determined by the price of SWATCH GROUP shares traded in the first line. Shareholders wishing to sell their shares can therefore either offer the shares to the company for the purpose of the subsequent capital reduction or sell said shares via the first line of trading. SWATCH GROUP shares will be quoted for the second line of trading in the main sector of the Swiss Stock Exchange from 23 February 1998.

6.2 Tax implications

The following tax considerations must be taken into account in respect of the second line of trading.

As far as federal withholding tax and direct tax are concerned, the repurchase of own shares for the purpose of a capital reduction is treated as a partial liquidation of the company making the repurchase. The implications of this for shareholders selling their shares are detailed below.

a) Withholding tax

Swiss federal withholding tax amounts to 35% of the difference between the repurchase price of the shares and their nominal value. The company making the repurchase, or the bank it has mandated, will deduct tax from the repurchase price for payment to the Federal Tax Administration. Shareholders domiciled in Switzerland are entitled to reimbursement of the withholding tax provided they are beneficial owners of the shares at the time they are surrendered (Art. 21, para. 1a of the Withholding Tax Law). Shareholders domiciled outside Switzerland may claim back the tax in accordance with any applicable double taxation agreements.

b) Stamp duty

The repurchase of own shares for the purpose of a capital reduction does not attract stamp duty. However, the stock exchange fee and Federal Banking Commission duty of 0.01% will apply.

c) Direct tax

The following applies to the levying of direct federal tax. Cantonal and municipal taxation procedures are, as a rule, the same as for federal tax.

· Shares held as private assets: For shares repurchased by the company, the difference between the repurchase price and the nominal value of the shares constitutes taxable income (nominal value principle).

· Shares held as corporate assets: For shares repurchased by the company, the difference between the repurchase price and the book value of the shares constitutes taxable profits.